Level playing field

Share this article

Neil Warren is concerned that many UK businesses selling goods should be registered for VAT in other EU countries

Key Points

What is the issue?

If a UK business sells goods to unregistered customers in another EU country, it might need to register for VAT there under the distance selling regulations

What does it mean to me?

Problems may arise if a business fails to monitor its sales into each EU nation and an overseas tax authority seeks arrears of tax if the business should have registered for VAT there

What can I take away?

There could be scope to register for VAT in another EU country on a voluntary basis and save tax if that on the goods in question is lower

Here is an opening teaser: what is the difference between a UK business selling £40,000 of goods each year to customers in Denmark who are not VAT-registered (usually private individuals) compared with one that sells the same goods to customers in Germany who also are not registered? The answer is that the business will charge Danish VAT on the sales to customers in Denmark but the UK rate to those in Germany. Why is this I hear some of you ask? Read on and all will be revealed.

Distance selling thresholds

The aim of EU VAT law is to create a level playing field between all Member States, so that a business has no competitive advantage being based in, say, Luxembourg, which has a low VAT rate of 17%, compared with one in, say, Sweden where the domestic rate is 25%. An important tool that helps to meet that aim is the distance selling rules, which can be summarised as follows:

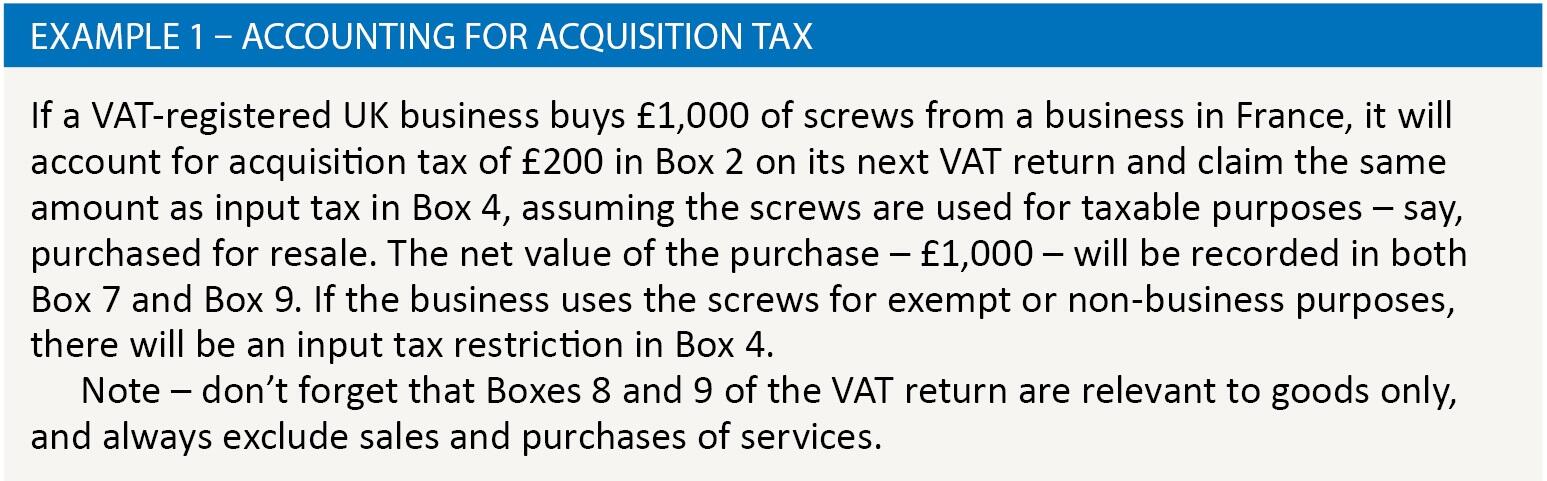

- If an EU-based business sells goods to a customer in another member state where the customer is VAT registered, the sale will be zero-rated. The customer will account for acquisition tax on his own VAT return based on the domestic rate that applies to the goods. The supplier must retain proof that the goods have left his country as a condition of zero-rating. He must also record the customer’s VAT number on his sales invoice(s) and a note instructing the customer to account for tax on his own return. See Example 1.

- If an EU-based business sells goods to an unregistered customer in another member state, domestic VAT is charged in the same way as if the customer were based in the supplier’s own country. However, the business must keep a record of total sales it makes to unregistered customers in each EU country by calendar year.

- If total sales into a country (only to customers without a VAT number) exceed its distance selling threshold, the supplier will cease to charge domestic VAT (which could happen part-way through a calendar month) and obtain a VAT number in the customer’s country. Future sales will then charge VAT according to the rate that applies in the customer’s country for the goods in question. These will be declared on VAT returns submitted to the overseas tax authority with the new registration.

- A member state can choose one of two thresholds for sales made into its country, either €35,000 or €100,000. Since the UK is outside the eurozone, the figure for EU businesses making sales to unregistered UK customers is £70,000 (VATA 1994, Sch 2, para 1).

As an aside, the countries with the higher rates of domestic VAT eg Denmark, Ireland and Sweden have opted for the lower threshold but those with lower rates eg France, Luxembourg and Germany have opted for the higher threshold (see ec.europa.eu for a full list). The references here to Denmark and Germany also answer my opening teaser.

There are a couple of important points to bear in mind. First, the turnover tests are carried out on a calendar year basis. So if you sold €99,999 of goods to unregistered customers in France in the 12 months to 31 December 2015, you have averted the need for a French VAT number and therefore start with a zero figure again on 1 January 2016. Second, it is important to be aware that sales to a business customer are included in the calculations if he does not have a VAT registration in his own country perhaps because he is trading below the domestic registration threshold. Sales to many charities or public bodies would also be included if they are not VAT-registered.

What if the limits are ignored?

My view is that many UK business owners (and some advisers) are unaware about the distance selling thresholds – or are aware of them but have forgotten to take them into account and review the relevant sales made to each EU country.

The idea for this article arose because the ATT VAT Sub-committee considered a story about how the tax authorities in Germany had identified that a UK business had been trading over the threshold there for many years, and had taken action to collect arrears. I had a similar situation to deal with a number of years ago involving a UK business selling golf club buggies into Ireland.

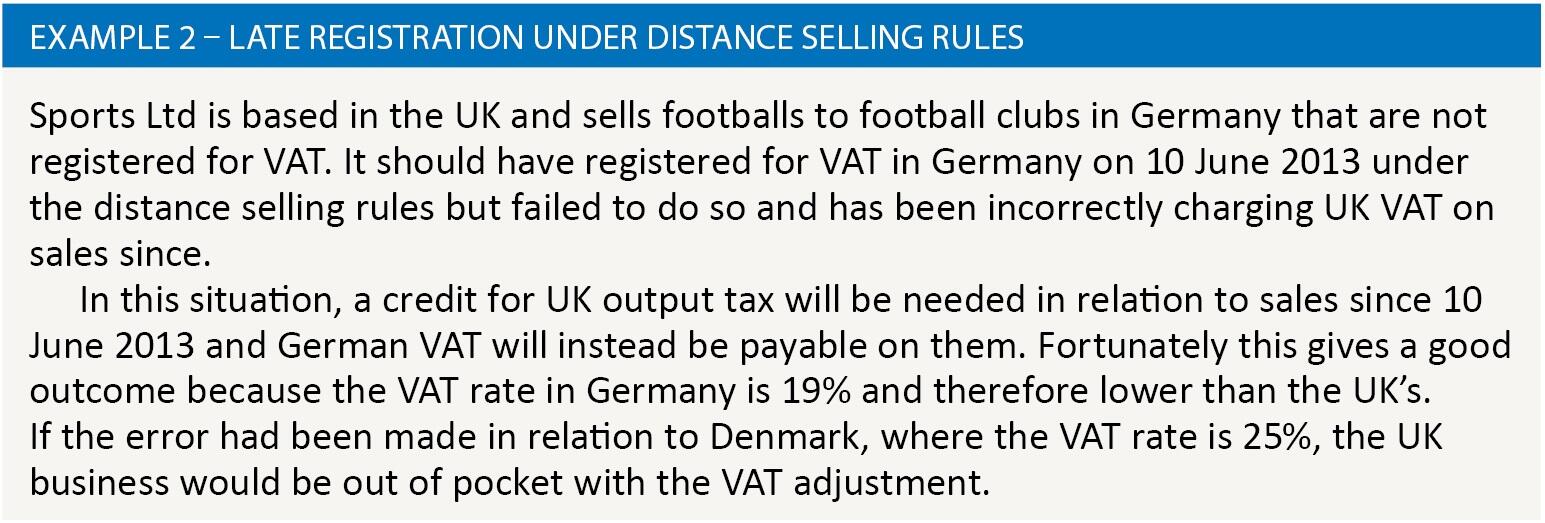

So what happens if a UK business has been charging UK VAT on its sales for many years into Germany, when it should have obtained a German VAT number and charged German VAT under the distance selling rules? See Example 2.

In the case of the golf club buggies, the problem arose in 2009 when the UK had a VAT rate of 15% and the Irish one was 21%. So a very annoyed supplier in Ireland reported the UK business to the Irish tax authorities because he was losing sales due to the VAT difference. All of which takes us back to the issue of the level playing field. The tax authorities in Dublin took up the mantle much as the Germans did. It was a big mess trying to sort out the arrears, and the 6% extra tax my client had to pay could not be recovered from customers in Ireland.

Accounting and VAT return issues

This is where things get tricky. Let us remain with the footballs scenario in Example 2:

- The UK business buys the balls from a UK supplier and is charged UK VAT. It will claim input tax on its UK VAT return in the normal way.

- The balls are stored at premises in London and then shipped directly to the German football clubs, with German VAT charged on the sales because of the distance selling rules.

If a UK business transfers goods to another EU state, where it owns or rents a warehouse from which it makes sales to customers there, it will usually need a VAT number in that second country. In such cases, the business is classed as making a supply of goods from its UK branch to its overseas branch at the time of the stock transfer, with acquisition tax accounted for by the overseas registration (see HMRC Notice 725, section 9).

However, in the case of distance sales – where the goods go directly from the UK premises to the customer – there is no acquisition tax payable through the overseas registration. In this case these entries are relevant on the respective VAT returns:

- UK VAT return: Box 6 and Box 8 entries are made to record the sale. Box 1 entry is unnecessary because output tax will be declared on the German return. If the business is registered for Intrastat, a declaration will also be made as a dispatch.

- German VAT return: output tax will be declared because German VAT has been charged and the net value of the sales will be recorded in the Box 6 equivalent of the return (the outputs box). An Intrastat entry as an arrival will be made if the business is registered so.

- There is no issue with EC Sales Lists, which need not be completed.

See HMRC Notice 725, para 6.17.

Final tips

Important as it is, this subject has become even more relevant in the modern trading world as online trading booms. Here are some pointers:

- Be aware that there is no distance selling threshold for goods that are subject to excise duty. These are always taxed in the country of destination. Therefore, an EU supplier that arranges the delivery of excise goods to a non-VAT registered customer in the UK must register for VAT here and vice versa (HMRC Notice 725, para 6.7).

- A business might decide to register under the distance selling rules before it has exceeded the €35,000 or €100,000 limits. There is no problem with such a voluntary registration and it might be sensible for a UK business to go down this route if the customer’s country has a lower VAT rate than the UK’s or perhaps applies a reduced rate to the goods in question. See HMRC Notice 725, para 6.10 to 6.13.