Non-deductible input tax: when can a claim still be made?

Share this article

We review the main items of expenditure where input tax cannot be claimed but highlight important exceptions where a claim can still be made.

Key Points

What is the issue?

Input tax cannot be claimed on business entertaining expenses and new cars in most cases. However, there are exceptions in the legislation, such as entertaining costs that relate to staff and the purchase of genuine pool cars. The article considers the conditions for making a valid claim.

What does it mean for me?

If goods are purchased that have a mixture of both business and private use, then input tax can be fully claimed in most cases, as long as output tax is declared on future VAT returns for private use over the life of the asset. This is known as the Lennartz mechanism.

What can I take away?

The Lennartz mechanism can only be adopted if there is some business use of an asset, linked to taxable supplies, and this can be as low as 1%. However, Lennartz cannot be used for purchases of some assets, which are highlighted in the article; e.g. ships and boats.

True or false? Input tax cannot be claimed on any expenditure that relates to business entertainment.

The initial answer to the above question would be ‘true’; however, an important challenge with VAT – and tax generally – is to understand when the various blocks in the legislation are overridden in some circumstances. I’ll highlight these situations in this article.

Entertaining staff

Imagine the following situation: Worthington Estate Agents has hired a box at a top sporting event and it will be occupied by a combination of partners, staff, customers and staff spouses. It will cost Worthington £10,000 plus VAT to include the game, a three course meal with champagne, a post-match cabaret and a free bar. The question to consider is: how much input tax can be claimed on the payment of £12,000 made to the event host for this top-quality entertainment package?

The answer is ‘it depends.’

- The first challenge is to establish the role of the staff. If they are able to enjoy themselves – free from any hosting duties with non-staff – then input tax can be claimed on their packages. This is because the entertaining of staff as a reward for their hard work – or future hard work – is classed as an expense with a business purpose and excluded from the input tax block on entertainment.

- If the staff must act as hosts for the non-staff – creating goodwill and potential orders from customers – the claim is blocked.

- Input tax on the expenses of the spouses and customers is blocked by virtue of the Value Added Tax (Input Tax) Order 1992.

- What about the partners? The starting point is that input tax on the entertaining costs of business owners is blocked but HMRC accepts that it can be claimed if an event is open to all or some staff, such as the office Christmas party.

See VAT Notice 700/65 para 3.2.

As a final twist to the tale, would it make any difference if any customers lived abroad? The answer is ‘yes’ for input tax purposes because there is an exception for the entertaining of overseas customers. However, the hospitality provided by Worthington would not – to quote from VAT Notice 700/65 para 2.6 – be classed as ‘reasonable in scale and character’, so output tax is payable on their entertainment, which will cancel the input tax gains.

Input tax can only be claimed on the costs of entertaining overseas customers – without an output tax liability – if the hospitality is limited to, say, coffee and sandwiches supplied at a business meeting. How mean is that!

Motor cars: what is a pool car?

The legislation blocks input tax claims if a new car is intended to be made available for private use. However, there is no problem with a business claiming input tax on the purchase of a car if it will be used as a tool of trade; e.g. by a driving school, taxi firm, car hire business or motor dealer. Input tax can also be claimed if a vehicle will be used as a genuine pool car that is available to all staff.

Over the years, I have received a lot of questions from clients about pool cars. For example: ‘One of our clients is buying a top-of-the-range BMW and paying a lot of VAT. Can we claim input tax if he keeps it at the office overnight and describes it as a “pool car” in the fixed asset register?’

My answer to the previous question would immediately be ‘no’ because the word BMW indicates it is not intended to be a run around pool car for the general use of all staff. No way! It is a prestige car that will be treated with kid gloves by its intended owner, usually the business owner or managing director.

There can be grey areas and input tax can be claimed if there is a genuine intention to use a vehicle as a pool car at the time it is purchased. However, HMRC’s guidance in its input tax manual at VIT52700 specifies three conditions that officers will consider:

- the vehicle is usually kept at the principal place of business;

- it is not allocated to an individual employee; and

- it is not kept at an employee’s home.

The important word to note – which is different to the word that officers will sometimes use when they are reviewing pool car issues – is ‘usually’ as opposed to ‘always’. In other words, the guidance states that a vehicle is ‘usually’ kept at, say, the office or warehouse of the business. This is different to the word ‘always’, which is less flexible.

Business gifts

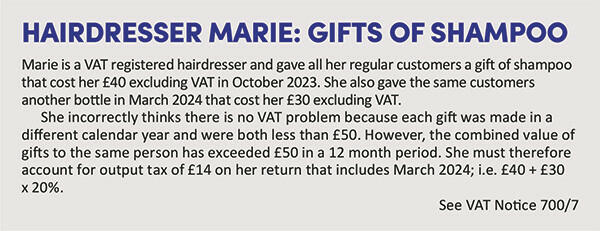

If a business provides a gift of goods for any business purpose – perhaps to reward a hardworking employee or loyal customer – it can claim input tax on the purchase of the goods. This assumes that there are no issues with partial exemption. However, when the goods are given away, this creates a tax point for output tax purposes on the value of the gift. The exception is if the cost of the gift and any other gifts given to the same person during the previous 12 months is less than £50 excluding VAT, in which case no output tax is due (see VAT Notice 700/7 s 2).

Here are some common mistakes with the business gift rules:

- If a business did not claim input tax on the purchase of the gift – perhaps because it was purchased from an unregistered supplier – there is no output tax liability when it is given away.

- The £50 limit excludes VAT and the test is applied on a rolling 12 month basis and not a calendar year or financial year basis.

- If the £50 limit is exceeded, output tax is due on all gifts made in that 12 month period.

See Hairdresser Marie: gifts of shampoo.

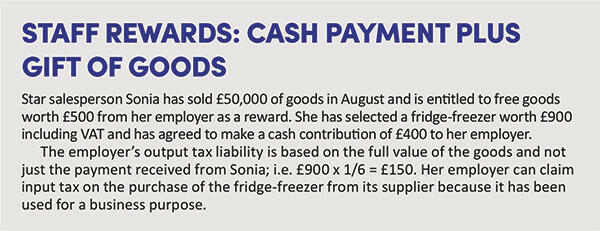

Rewarding staff

Unfortunately, there is no difference in the rules for gifts made by a business to its staff; e.g. a reward to sales staff who meet certain targets. In other words, output tax will be payable at the time they are given away if the £50 limit is exceeded.

However, there is a further issue to consider if the staff member can make a cash payment to get more goods. See Staff rewards: cash payment plus gift of goods.

The £50 limit does not apply to a gift of services and output tax is always payable on the onward supply of the services to the recipient. So, for example, if a business has purchased a package from a local golf club that includes 18 holes of golf and a three-course meal for £800 plus VAT, it can claim input tax on the invoice from the golf club but output tax of £160 will be due on the onward supply to the employee.

Business or private expense?

What is the difference between the purchase of goods that have 1% intended business use and 99% intended private use, compared to another item that has 100% private use?

The answer is that a business can fully claim input tax if there is some business use – even if it is only 1% – and then account for output tax on the private use of the goods over their economic life.

However, if an expense is wholly for private purposes, input tax is fully blocked because there is no business use.

The output tax option is known in VAT speak as the Lennartz mechanism and is an alternative to the traditional method of apportioning input tax at the time of purchasing the item in question. There is no de minimis limit, hence why 1% business use is fine. However, there is a further twist: the Lennartz option is not available for ships, boats, other vessels, land and property, and aircraft.

To share a final tale, I was recently asked if a business could claim input tax on the purchase of a director’s expensive watch if the company bought the item and capitalised it to its balance sheet and also declared it as a benefit-in-kind of the director?

This question highlights an important point that action taken by a business in relation to direct tax has no bearing on decisions about VAT. The reality is that the director’s watch has no business purpose, so input tax is fully blocked on the purchase price.