A wide view

Share this article

Helena Kanczula and Robert Harness examine the transactions in land rules introduced by FA 2016

Key Points

What is the issue?

Finance Act 2016 replaced the ‘transactions in land’ rules with an entirely new set of provisions, which include widely-drafted anti-enveloping and anti-fragmentation rules.

What does it mean to me?

The transactions in land rules ensure that where UK land (or property deriving its value from UK land) is disposed of as part of an arrangement that is, in substance, a trading transaction, any profit or gain will be taxed as trading income. The changes are therefore relevant to anyone with an interest in the sale or development of UK property.

What can I take away?

Wherever UK property is held and an intention to sell it exists, the rules may apply. Existing arrangements should be carefully reviewed.

Background

Finance Act 2016 replaced the previous transactions in land (‘TIL’) rules with entirely new legislation, broader in scope than before.

The changes were introduced as part of a package of measures designed to prevent offshore structures being used to reduce or eliminate the UK tax payable in respect of UK property development profits. These measures have therefore largely been discussed to the extent that they affect offshore arrangements.

However, the TIL changes will apply to UK companies and individuals just as much as non-resident ones, and so are relevant to anyone with an interest in the sale or development of UK property.

Transactions in UK land

The transactions in land rules, both in their current and former incarnations, ensure that where UK land is held for what is effectively a trading purpose, its disposal will be treated for UK tax purposes as an income – rather than a capital – transaction.

More specifically, any gains (or losses) arising on the disposal of UK land will be treated as trading income (or losses) if:

- the land was acquired or developed with the main purpose (or one of the main purposes) being to realise a profit or gain on disposal;

- property deriving its value from the land was acquired with the main purpose (or one of the main purposes) being to realise a profit or gain on disposal; or

- the land has been held as trading stock.

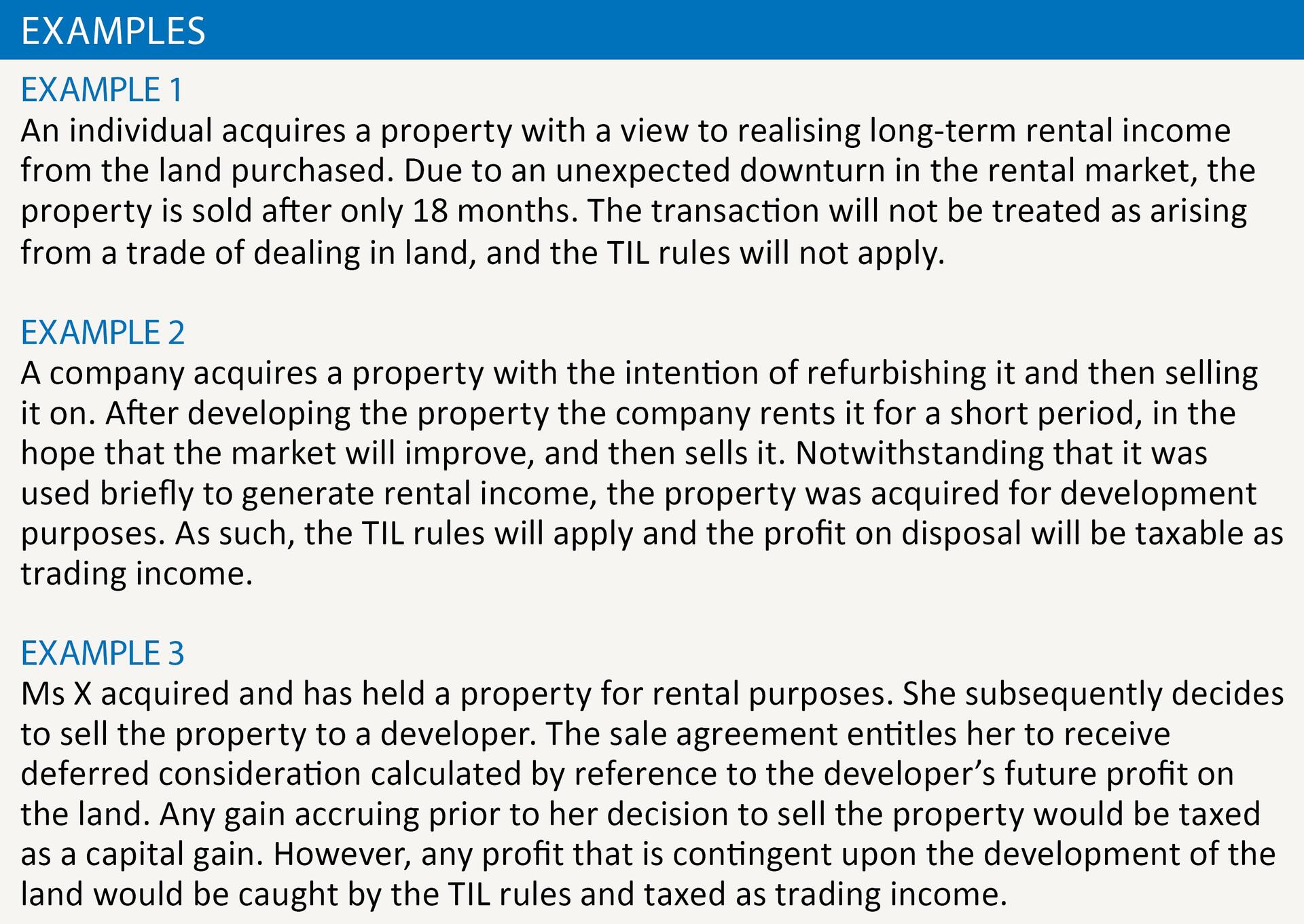

Any profit attributable to periods before the intention to develop or sell the land was formed does not fall within the TIL rules and so should still be within the capital gains tax rules.

It is noted that the ‘sole or main object’ test in the previous TIL legislation has been replaced: realising a profit on disposal now only needs to be ‘one of the main purposes’. This raises the possibility that the new rules will apply to a broader range of transactions, as almost any property investment will be made with a potential future disposal in mind.

However, HMRC’s new guidance (at BMI60555) makes clear that ‘the legislation should always be understood in the context that it is taxing only what are, in substance, trading profits’. Numerous examples are provided (at BIM60560) to illustrate when the rules will bite; however, in general where a property is acquired and held with the intention of realising long-term rental profits and/or capital appreciation, the rules should not apply.

In practice, then, the change of wording is unlikely to have any meaningful impact to properties genuinely held as investments. However, the retention of documentation by investors, to confirm whether or not those intentions have changed, is as important as ever.

The more noteworthy changes to the TIL rules are represented by the revised anti-enveloping provisions and anti-fragmentation rules, described in more detail below. It should also be noted that the new TIL legislation no longer permits an advance clearance procedure.

Anti-enveloping rule

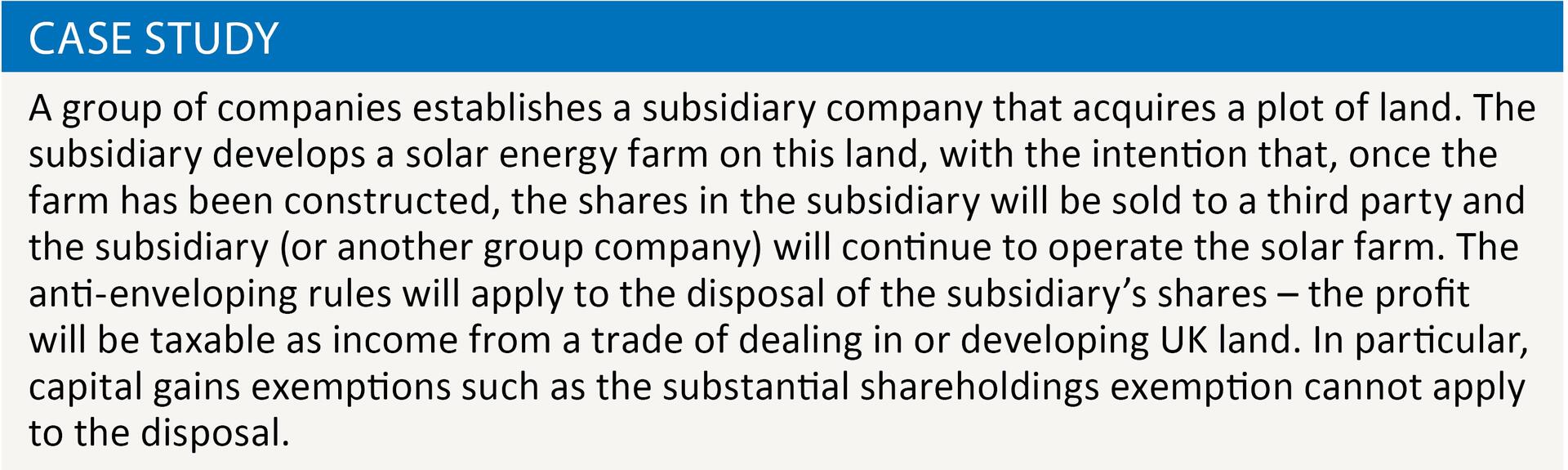

The anti-enveloping provisions prevent property traders and developers from avoiding a charge to income by selling assets that derive their value from land, rather than selling the land itself. The typical example (but by no means the only one) would be where shares in a property-holding company are sold.

Although this kind of anti-enveloping measure existed before, the new rule has a much broader scope and applies when a person:

- disposes of any property that (at the time of the disposal) derives at least 50% of its value from UK land; and

- is ‘a party to, or concerned in, an arrangement’ relating to that land, and the main (or one of the main purposes) of that arrangement is:

- to deal in or develop the land; and

- realise a profit or gain from a disposal of property deriving whole or part of its value from that land.

Some observations applicable to investors in property dealing or development companies:

- Under the new rules, minority shareholdings in property dealing and development companies are potentially within scope.

The anti-enveloping rule under the old TIL legislation applied only where there was also a disposal of control over the land. Now the rules are in point whenever UK land represents the majority of value disposed of. (For this purpose, value can be traced through any number of companies, partnerships, trusts or other entities or arrangements.) - Because the disposing person must be ‘involved in an arrangement’ to deal in or develop the underlying land, they must be more than a mere passive investor.

To be concerned in an arrangement it is necessary to be acting together in some way or to have knowledge of the purpose of the arrangement. In most cases, it should be straightforward to determine whether this threshold is met. - HMRC guidance (BIM60595) makes clear that there should be no double taxation of trading profits. Where shares in a company are disposed of and all of the company’s UK land is held as trading stock that would be subject to UK tax if sold, the TIL rules should not apply.

Anti-fragmentation rules

In the absence of specific provisions, a developer/dealer could minimise the profit subject to the TIL rules by paying fees to an associated service provider. The new anti-fragmentation provisions counteract such arrangements.

Where a ‘relevant contribution’ to the development or disposal of land is made by a person associated with the developer/dealer either during the project life or during the six months after the disposal of the land, any profit made by the associated entity in relation to that contribution is included in the amount taxed under the TIL rules.

For this purpose:

- a ‘relevant contribution’ includes any contribution to the development or disposal of the land. In particular, it includes the provision of services and the provision of finance that involves the assumption of risk; and

- the definition of ‘associated’ is widely drawn – for example, two companies can be associated where one has a 25% interest in one or a third party holds a 25% interest in both.

The anti-fragmentation rules can apply to payments of interest even where the interest is calculated at an arm’s length rate. The determining factor is whether a risk premium is reflected in the interest, so that the lender assumes a portion of the project risk, or whether the loan allows the lender to participate in the project profit. In these cases, the interest payments will be caught by the rules.

If the contribution made by the associated entity is insignificant by reference to the overall size of the project, then it is disregarded. ‘Insignificant’ for this purpose is not defined; however, HMRC have indicated that services adding limited value (the example given is admin services charged on a cost-plus-2% basis) will generally fall outside the anti-fragmentation rules.

Image

Final thought

Historically, the TIL provisions have rarely been invoked by HMRC. However, the nature of the changes made – and the context in which they have been made – suggests that these rules will be applied more frequently in the months and years to come.